Bilanol/iStock via Getty Images

Let’s start with the obvious. Coal prices are hitting new highs on the back of the global energy rush following post-pandemic economic reopenings and disruptions from Russia’s weaponization of energy. EU the sanctions have all but shut Russian coal off its continent and exacerbated a global scramble for rock. Thermal coal also remains important for power generation around the world. India uses it for 70% of its total electricity needs and China is looking to add 270 GW of coal-fired thermal capacity over the next five years to 2025. Even Germany, Europe’s largest economy, has shifted more heavily to coal in recent months as shutdowns of its nuclear power plants progress.

Looking for Alpha

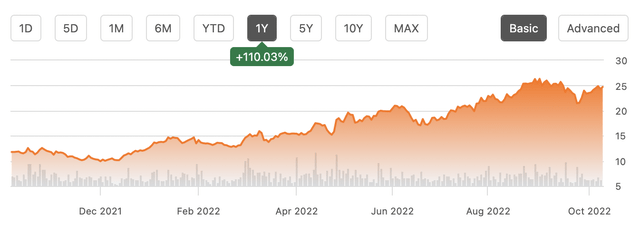

Alliance Resource Partners based in Tulsa, Oklahoma (NASDAQ: ARLP) now benefits from a near-generational intersection of unique geopolitical events and political failures. Indeed, coal prices in the United States reached a record high above $200/tonne. The party has arrived for thermal coal investors with an increased quarterly dividend payout and positive capital gains fully in lyrical rhythm. However, market sentiment failed to take into account the bigger picture, and while the ESG movement may have been too euphoric about its initial timelines for renewables adoption on the track, the deal recently signed Inflation Reduction Act represents a sea change for the industry. To be clear, coal remains fundamentally incompatible with the march to net zero. The law aims to allocate at least $370 billion to accelerate the march to net zero over the next decade.

Coal bulls need to understand that this is not the fringe dream of a small number of environmentalists. It represents what is quickly becoming the most defining change in contemporary American history. The Inflation Reduction Act is simply unprecedented in its scope and scale and represents the most relevant effort by any government on earth and at any time in human history to strongly sway the winds of change to its entire energy system. The incentives included in the law go beyond the initial cost of $370 billion. They will quickly become the ignition that will see coal’s contribution to the US electric grid continue to decline permanently.

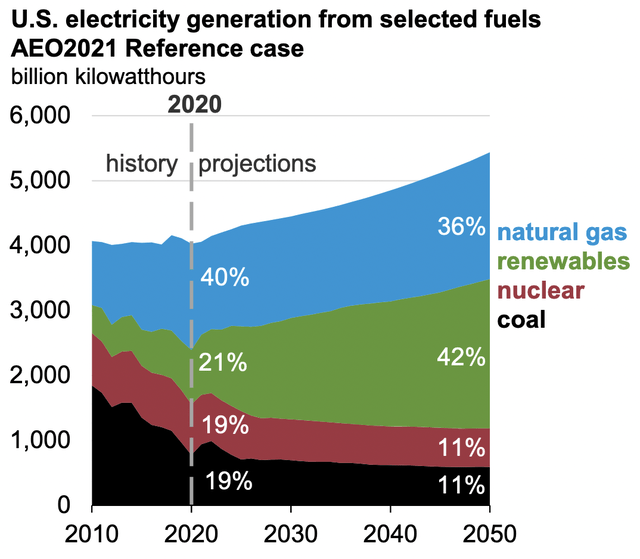

US demand for coal erodes as renewables become even cheaper

Coal’s contribution to the US electric grid has been in structural decline since the start of the new millennium as natural gas took over and renewables experienced explosive growth of a few hundred MW in the 1990s.

Energy Information Association

Credit Suisse analysts at the end of October published a research note on the law that highlights how staggering its reach is. First, the law could spend twice as much as the currently planned figure of $370 billion, because many important provisions, including subsidies for solar and large-scale battery storage systems, are uncapped tax credits. .

Essentially, the US government wrote a blank check to the renewable energy industry. The frequently quoted figure is wrong. As long as a project meets the conditions, the government will provide credits. There is no upper limit, no budget and no restrictions. Total spending for the law is expected to be over $800 billion, twice the frequently quoted figure. Taking into account the pull effects of private capital in addition to government subsidies, the total capital allocated to technologies that directly compete with coal could reach $1.7 trillion over the next decade to 2032.

Advisors from the Boston Consulting Group estimated that the incentives included in the law could increase the deployment of zero-carbon energy to up to 80% of electricity generation as early as 2030. This would be ahead of the Energy Information Association chart and would see coal fall to single digit percent by the end of this decade. US solar and wind by 2029 could be the cheapest in the world at less than $5 per MWh due to law, with utility-scale solar deployments alone expected to increase by 40%, or about 62 GW, over pre-IRA projections through 2027.

So, as ESG orthodoxy is beleaguered by the boom in coal and oil in this particular and unique time, it is set to flourish again. America’s seemingly shaky zero-carbon transition has been resurrected with the terms of the law that can only be described as an 800-pound gorilla crushing anything that doesn’t meet its scope and requirements.

The party will come to an end but not before the risks

Alliance Resource Partners saw its market cap hit $3.10 billion due to rising coal prices. However, the company’s broader valuation is understandably still quite supportive of its bulls with its price to 12-month non-GAAP earnings multiple at 10.34x. Although this figure is above its sector median, it drops to 5.11x when forward earnings are taken into account.

Looking for Alpha

This represents the most relevant risk for a bearish contrarian view of society. Financials are improving with revenue reaching $616 million for its second quarter of fiscal 2022, up 70.1% from the year-ago quarter. Coal prices could remain at their elevated levels for years, supporting higher dividend payouts and additional common stock gains.

Looking for Alpha

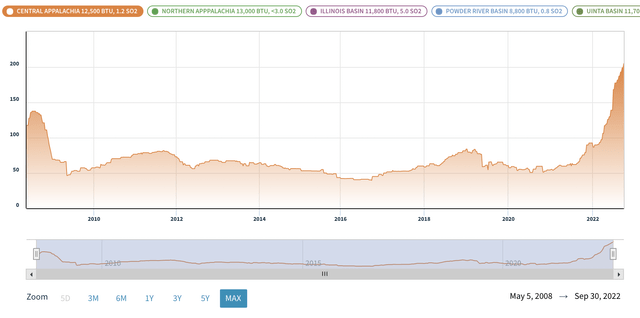

But the current push appears to ignore the existential risk posed to Alliance Resource Partners in an economic direction that leaves no room for coal. The Cut Inflation Act is intended to be a fundamental part of the US effort to reduce greenhouse gas emissions. Against this future, current dividends and capital gains will prove transitory. The law places a significant fiscal safety net for the structural shift to zero-carbon technologies and Alliance Resource Partners will likely find itself falling behind as the current unique conditions give way and coal prices fall to make way for a zero-carbon future. . I would not advise investors to sell short using stocks, but rather via longer-term out-of-the-money put options. I would go with Jan 19, 2024 and any strike price from $20 and below.

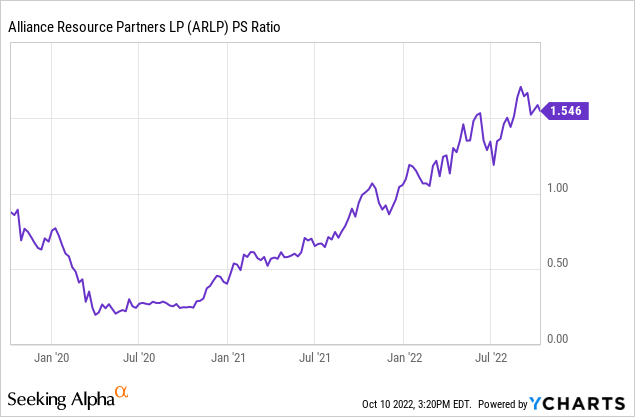

Assuming the short thesis plays out, the company’s P/S ratio should return closer to its recent lows. This could reduce the current 1.5x multiple to 0.5x. This would be set against coal prices falling more than half from their historical average.

Nasdaq Data Link

This would lead to a reduction of more than 75% in coal prices. Faced with these two factors of falling multiples and falling coal prices, Alliance Resource Partners should see trailing 12-month revenues return to where they were at the start of its 2020 financial year. This would see the company’s valuation return less than $1 billion on revenue. of approximately $1.5 billion and would represent a reduction of more than 60% from the current price of $23.89 per common share.

/cloudfront-us-east-1.images.arcpublishing.com/tgam/RUTZATCRJVIS3JHFJRCDKRJ6IA.JPG)

{kind=link}

{kind=link}

{kind=link}